Understanding Whole Life Insurance: Benefits, Features, and Costs

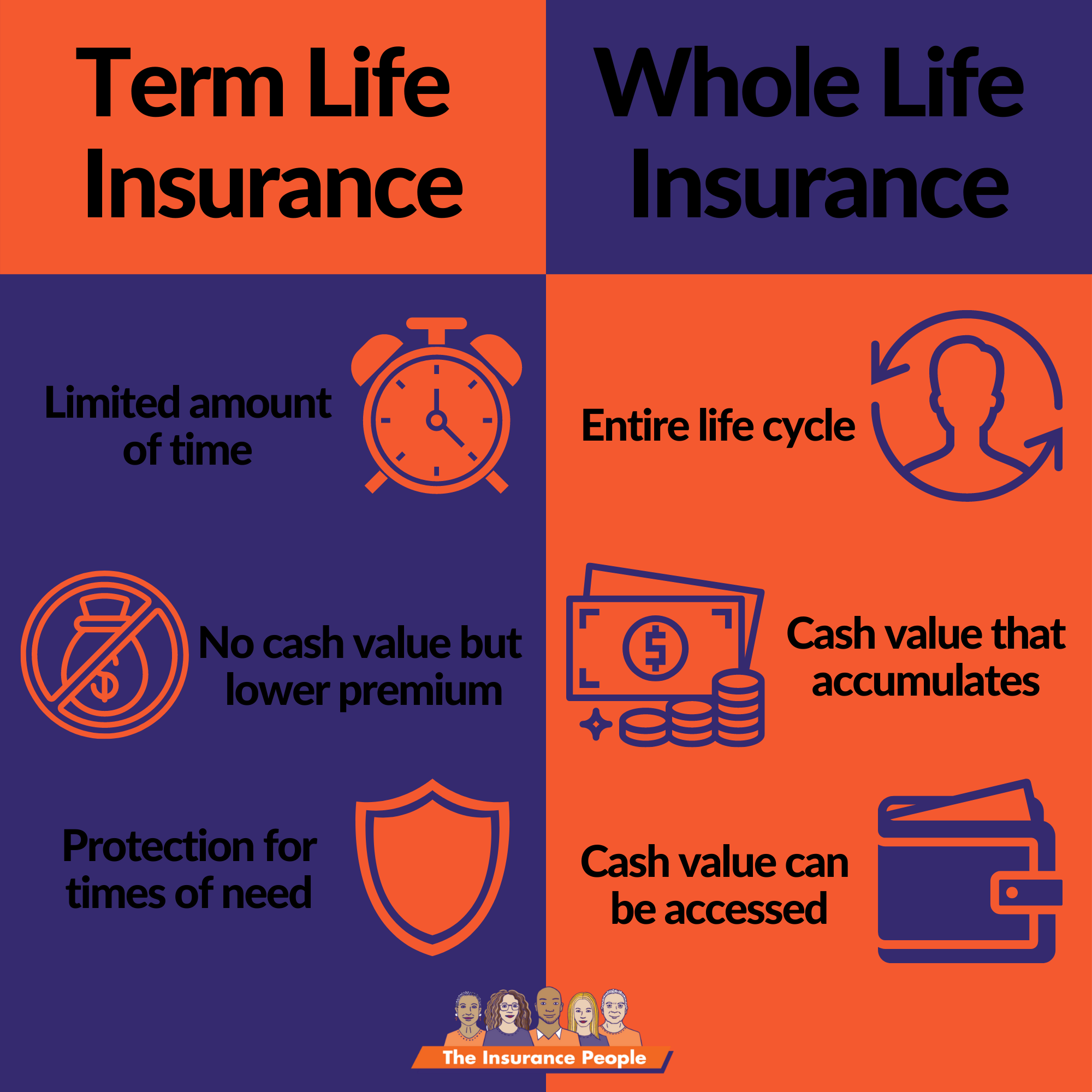

Whole life insurance is a type of permanent life insurance designed to provide lifelong coverage with a focus on both protection and savings. One of the primary benefits of whole life insurance is its consistent premium payments, which remain the same throughout the policyholder's life. Additionally, this insurance type builds cash value over time, allowing policyholders to borrow against it or withdraw funds if needed. Other advantages include guaranteed death benefits, which reassure beneficiaries and contribute to financial security, and potential dividends, which can enhance the policy's value.

When considering whole life insurance, it's essential to understand its features and costs. Policies typically offer a cash value component that grows at a fixed rate, but this growth can be slower compared to other investment options. Costs associated with whole life insurance are generally higher than term life insurance due to the lifelong coverage and cash value benefits. Factors influencing the cost include age, health status, and the amount of coverage desired. In sum, while whole life insurance can be a valuable financial tool, evaluating both its benefits and costs is crucial in making an informed decision.

Is Whole Life Insurance the Right Choice for Your Financial Future?

When considering your financial future, one option that often comes up is whole life insurance. Unlike term life insurance, which only offers coverage for a specific period, whole life insurance provides lifetime protection and includes a cash value component that grows over time. This dual benefit can serve as a crucial part of your overall financial strategy. In fact, the cash value can be borrowed against or withdrawn, providing a potential source of funds for emergencies or investment opportunities.

However, it's essential to evaluate whether whole life insurance aligns with your long-term financial goals. While it can offer stability and peace of mind, the premiums tend to be significantly higher than those of term life policies. Consider factors such as your current financial situation, your family’s needs, and other investment avenues before making a decision. Conducting a thorough assessment will help ensure that you choose the right policy that not only provides coverage but also contributes to your financial growth.

5 Key Reasons Why Whole Life Insurance is Your Ultimate Safety Net

Whole life insurance serves as a critical financial safety net for individuals and families seeking long-term security. One of the primary reasons to consider this type of insurance is its ability to provide a guaranteed death benefit. This means that, regardless of market fluctuations or changes in personal circumstances, your beneficiaries will receive a predetermined sum upon your passing. Additionally, whole life policies accumulate cash value over time, allowing you to borrow against this amount or withdraw it if necessary, providing peace of mind for unexpected expenses.

Another key factor is the predictably stable premiums. Unlike term insurance, which may require higher payments as you age, whole life insurance locks in your premium rate for the duration of the policy. This can be particularly beneficial for budgeting and financial planning. Lastly, whole life insurance can serve as a formidable estate planning tool. It enables individuals to leave a financial legacy, ensuring that heirs receive the support they need, while also potentially covering estate taxes. In sum, investing in a whole life insurance policy can create a reliable financial foundation for both you and your loved ones.